- ENQUIRE ONLINE OR CALL US

- 08 8451 1500

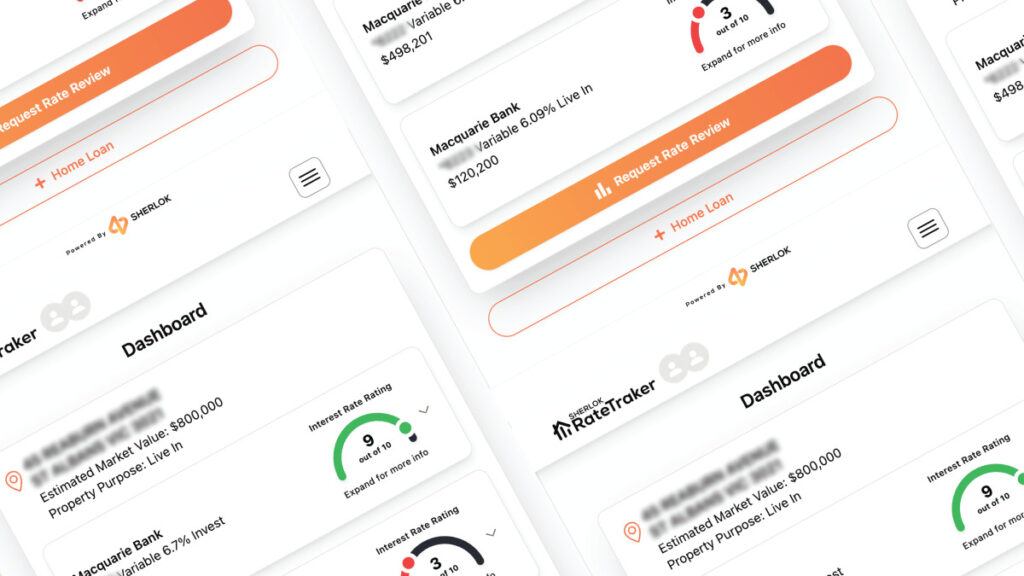

New Tool – Track your interest rates in real-time…

Major ATO Tax Change for Property Sellers from Jan 1

At its meeting today, the RBA Board decided to leave the cash rate unchanged at 4.35 per cent.

Statement by RBA’s Michele Bullock:

At its meeting today, the Board decided to leave the cash rate target unchanged at 4.35 per cent and the interest rate paid on Exchange Settlement balances unchanged at 4.25 per cent.me.

Underlying inflation remains too high.

Inflation has fallen substantially since the peak in 2022, as higher interest rates have been working to bring aggregate demand and supply closer towards balance. Measures of underlying inflation are around 3½ per cent, which is still some way from the 2.5 per cent midpoint of the inflation target.

The most recent forecasts published in the November Statement on Monetary Policy (SMP) do not see inflation returning sustainably to the midpoint of the target until 2026. The Board is gaining some confidence that inflationary pressures are declining in line with these recent forecasts, but risks remain.

The outlook remains uncertain.

While underlying inflation is still high, other recent data on economic activity have been mixed, but on balance softer than expected in November.

Growth in output has been weak. National accounts for the September quarter show that the economy grew by only 0.8 per cent over the past year. Outside of the COVID-19 pandemic, this is the slowest pace of growth since the early 1990s. Past declines in real disposable income and the ongoing effect of restrictive financial conditions continued to weigh on household consumption spending, particularly on discretionary items.

A range of indicators suggest that labour market conditions remain tight; while those conditions have been easing gradually, some indicators have recently stabilised. The unemployment rate was 4.1 per cent in October, up from 3.5 per cent in late 2022. That said, employment grew strongly over the three months to October, the participation rate remains close to record highs, vacancies are still relatively high and average hours worked have stabilised. At the same time, some cyclical labour market indicators, including youth unemployment and underemployment rates, have recently declined.

Wage pressures have eased more than expected in the November SMP. The rate of wages growth as measured by the Wage Price Index was 3.5 per cent over the year to the September quarter, a step down from the previous quarter, but labour productivity growth remains weak.

Taking account of recent data, the Board’s assessment is that monetary policy remains restrictive and is working as anticipated. Some of the upside risks to inflation appear to have eased and while the level of aggregate demand still appears to be above the economy’s supply capacity, that gap continues to close.

The central projection is for growth in household consumption to increase as income growth rises. September quarter data suggest that both incomes and consumption had recovered a little slower than forecast, but more recent information has suggested a pick-up in consumption in October and November. There is a risk that any pick-up in consumption is slower than expected, resulting in continued subdued output growth and a sharper deterioration in the labour market. More broadly, there are uncertainties regarding the lags in the effect of monetary policy and how firms’ pricing decisions and wages will respond to the slow growth in the economy and weak productivity outcomes at a time of excess demand, and while conditions in the labour market remain tight.

There remains a high level of uncertainty about the outlook abroad. Most central banks have eased monetary policy as they become more confident that inflation is moving sustainably back towards their respective targets. They note, however, that they are removing only some restrictiveness and remain alert to risks in both directions, namely weaker labour markets and stronger inflation. Geopolitical uncertainties remain pronounced.

Sustainably returning inflation to target is the priority.

Sustainably returning inflation to target within a reasonable timeframe remains the Board’s highest priority. This is consistent with the RBA’s mandate for price stability and full employment. To date, longer term inflation expectations have been consistent with the inflation target and it is important that this remains the case.

While headline inflation has declined substantially and will remain lower for a time, underlying inflation is more indicative of inflation momentum, and it remains too high. The November SMP forecasts suggest that it will be some time yet before inflation is sustainably in the target range and approaching the midpoint. Recent data on inflation and economic conditions are still consistent with these forecasts, and the Board is gaining some confidence that inflation is moving sustainably towards target.

The Board will continue to rely upon the data and the evolving assessment of risks to guide its decisions. In doing so, it will pay close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market. The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that outcome.

Need help with your finances or want to discuss how interest rate changes could affect your situation? We’re as close as your phone – call 08 8451 1500

Sam, Matt & Team

Urbantech Finance

>> See all of our best home loan rates here + a lot more…

{kind=link}

{kind=link}

{kind=link}